M2P Fintech

Fintech is evolving every day. That's why you need our newsletter! Get the latest fintech news, views, insights, directly to your inbox every fortnight for FREE!

Credit cards continue to be a cornerstone of digital payments. In 2025, credit card applications reached their highest levels with millions of customers especially younger demographics, actively seeking new credit options. The global credit card market is projected to surpass USD 115 billion by 2026 and continue growing steadily to nearly USD 153 billion by 2035.

In this rapidly evolving market, fintechs and issuers are prioritizing differentiation to capture consumer loyalty. Co-brand and co-badge credit cards are emerging as powerful strategies to unlock unique value propositions, engage new customer segments, and drive competitive advantage. As issuers and brands leverage advanced technologies like AI-driven security and open infrastructure to deliver these specialized products, understanding the nuances between offerings like co-brand and co-badge credit cards becomes essential for both businesses and consumers alike.

Let’s break it down.

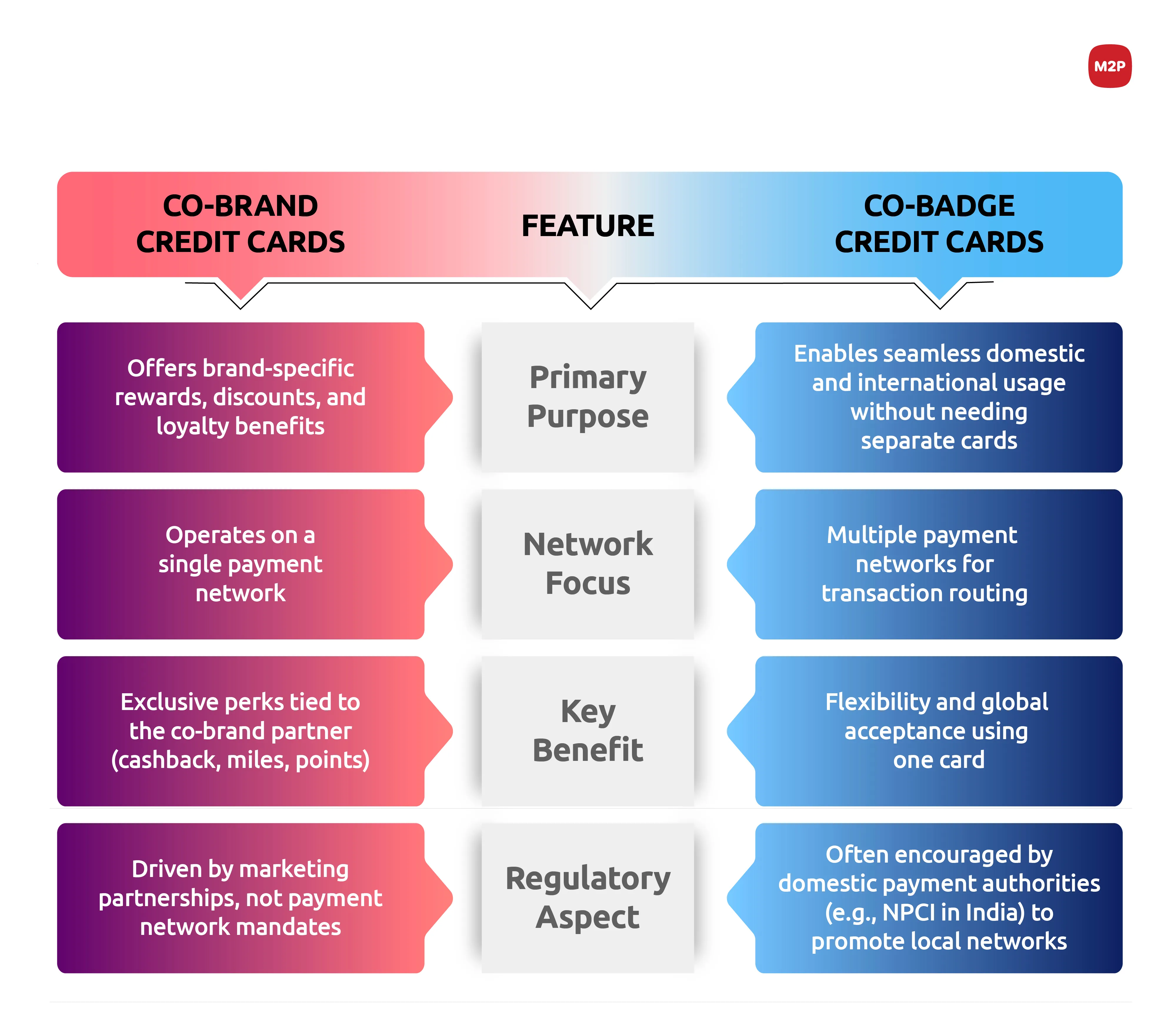

A co-brand credit card is a strategic partnership between a licensed card issuer (usually a bank) and another entity such as a consumer brand, fintech, or even another bank. The licensed issuer is mandatory because it ensures compliance with regulatory and network requirements. The card carries the branding of both the issuer and the partner brand (e.g., an airline, retailer, or hotel chain).

The main objective is to leverage the partner brand's existing customer base and loyalty, driving engagement, and repeat business for both entities. For the customer, it offers exclusive rewards, discounts, or perks that enhance their experience with that specific brand.

Federal Bank partners with Scapia to create a card designed for travelers with zero forex markup, airport lounge access and reward coins for travel booking. Powered by Visa for global acceptance, the card ensures seamless, secure transactions worldwide, making it the perfect companion for frequent travelers.

A co-badge credit card is a single card that operates on two payment networks simultaneously. For instance, in India, a credit card issued on the domestic payment network is often co-badged with an international network. This means that when you use the card in India, transactions are processed via the domestic payment network, but when you use the same card internationally, the transactions are processed through the global network.

Such an arrangement allows seamless acceptance of the card both domestically and globally, ensuring convenience for the cardholder while leveraging the local network for domestic use and the global network for international usage. In essence, a co-badge card provides the flexibility of using one card worldwide, with transactions routed through the most appropriate network depending on the location.

Several credit card implementations leverage a dual-network architecture. Domestic transactions are routed through local payment rails to optimize cost and processing efficiency, while international transactions are automatically switched to a global network layer that supports acceptance across multiple international markets through its extended acceptance ecosystem.

Issuers opting for co-badge credit cards must manage the technical and operational requirements suited for the dual network support (e.g., a domestic network alongside an international one). This dual network setup translates directly into:

Incremental Certification Efforts: Ensuring full compliance and certification with the technical standards and regulations prescribed for a dual network support.

Dual operations management: Operational teams manage dual settlement processes, dispute resolution protocols, and chargeback management flows, demanding a more sophisticated operational infrastructure. Automated reconciliation platforms such as Recon 360 from M2P can handle this with little to no incremental resourcing.

But beyond operational complexity, the real battleground for differentiation lies in how the co-brand and co-badge credit card shape the customer experience. Understanding the fundamental differences between co-brand and co-badge credit cards is crucial, so let’s take a closer look at what sets them apart in the next section.

Understanding these differences is critical, but the real differentiator lies in how issuers leverage each model to drive acquisition, loyalty, and profitability aligning with their unique business objectives.

Understanding these differences is critical, but the real differentiator lies in how issuers leverage each model to drive acquisition, loyalty, and profitability aligning with their unique business objectives.

Low Customer Acquisition Cost: FIs can leverage the partner brand's existing, loyal customer base to acquire new cardholders at a significantly lower cost than traditional marketing efforts.

Enhanced Customer Loyalty: Co-brand credit cards typically have lower attrition rates because customers are loyal to both the bank's financial product and the partner's rewards program.

Increased Share of Wallet: These cards incentivize customers to consolidate their spending with the partner brand and, by extension, the issuing bank, increasing the overall transaction volume.

Access to Valuable Data Insights: Partnership agreements often allow for valuable data sharing, providing the bank with deeper insights into specific consumer spending behaviors (e.g., travel patterns, retail preferences).

Enhanced Brand Visibility and Trust: By associating with reputable and popular brands, FIs can boost their own brand visibility and build trust with new customer segments.

Optimized Interchange Fees: Ability to route domestic transactions through a local network which typically has lower interchange fees, directly improving the FI's margins.

Universal Acceptance Assurance: Combining a local network with strategic international networks guarantee the card works universally across all merchant infrastructures, reducing customer frustration from declined transactions.

Reduced Scheme Fees: Financial institutions may benefit from reduced overall network scheme fees or favorable terms when they commit a certain volume of domestic transactions to the local network partner.

Accelerated Rewards: Earn significantly higher points or cashback when spending it with the specific partner brand (e.g., airline, hotel, retailer).

Exclusive Perks: Receive tangible, brand-specific benefits like free checked luggage, complimentary hotel nights, annual free movie tickets, or loyalty status upgrades.

Instant Redemption: Easily use points for immediate discounts at the partner brand's stores or websites.

Universal Acceptance: Guaranteed payment success using either a local network or a major international network on a single card.

Payment Flexibility: The ability (often automated) to choose which network processes the transaction, optimizing acceptance or cost.

Potential Cost Savings: Access to lower transaction fees for domestic purchases if routed through a local network, sometimes translating to better discounts or lower fees for the user.

Seamless International Travel: Ensures the card works smoothly both domestically and while traveling abroad, without needing a separate card.

While seamless international usage elevates the customer experience, the real challenge for issuers lies in navigating the strategic implications for co-badged credit cards.

Financial institutions may consider launching co-badge credit cards when targeting diverse markets where customers demand strong domestic presence and international usability. This type of card is especially beneficial for issuers focusing on cross-border travelers, migrant populations, or regions with multiple prevalent card schemes.

The decision to pursue co-badge depends on strategic objectives:

Market Access: If a financial institution’s goal is to serve regional markets while maintaining broad global acceptance, co-badge allows to combine a local network’s reach with a global network.

Enhanced Customer Experience: Co-badge credit cards offer users flexibility in transaction routing, access to diverse offers, and higher acceptance in both domestic and international merchants, enhancing overall satisfaction.

Ultimately, by aligning your target demographics, geographic focus, and operational capabilities with these considerations, financial institutions can make a well-informed decision on adopting a co-badge strategy.

The payments sector is continuously evolving, shaped by new regulations, network strategies and shifting changing consumer expectations. At M2P, we stay ahead of these shifts to ensure our solutions remain cutting-edge.

Our comprehensive Credit Stack has already powered co-brand credit card programs, enabling banks and fintechs to deliver personalized, brand-driven card experiences. We also support co-badge credit cards, reflecting the latest industry trends and compliance needs. This comes along with cost optimizing product architecture that helps financial institutions and brand partners choose the co-badge and keep the costs closer to domestic transactions.

This seamless integration of co-brand and co-badge credit card capabilities within a single, API-driven platform empowers financial institutions to offer versatile, future-ready card products that meet diverse customer and market demands.

If you’re a bank or fintech looking out to launch co-badge credit cards, Contact us today for a demo and start building the next generation of credit card experience.

Follow us on LinkedIn and Twitter for insightful fintech bytes curated for curious minds like you.

Source

https://www.businessresearchinsights.com/market-reports/credit-card-market-118933

Fintech is evolving every day. That's why you need our newsletter! Get the latest fintech news, views, insights, directly to your inbox every fortnight for FREE!