M2P Fintech

Fintech is evolving every day. That's why you need our newsletter! Get the latest fintech news, views, insights, directly to your inbox every fortnight for FREE!

Financial fraud is no longer confined to traditional banking systems—it has expanded into fintech, crypto, e-commerce, and cross-border ecosystems. As fraud evolves, so do regulations. In 2026, compliance teams face a rapidly changing global regulatory environment where expectations are stricter, more technology-driven, and highly outcome-focused.

Governments and regulators are not just asking, “Do you have controls?”—they are asking, “Are your controls actually effective?” This shift is redefining how organizations approach fraud prevention, AML (Anti-Money Laundering), and risk management.

Fraud regulation globally is largely anchored in AML and KYC frameworks, guided by international standards such as the Financial Action Task Force (FATF) recommendations. These recommendations form the baseline adopted by most countries to combat money laundering and terrorist financing.

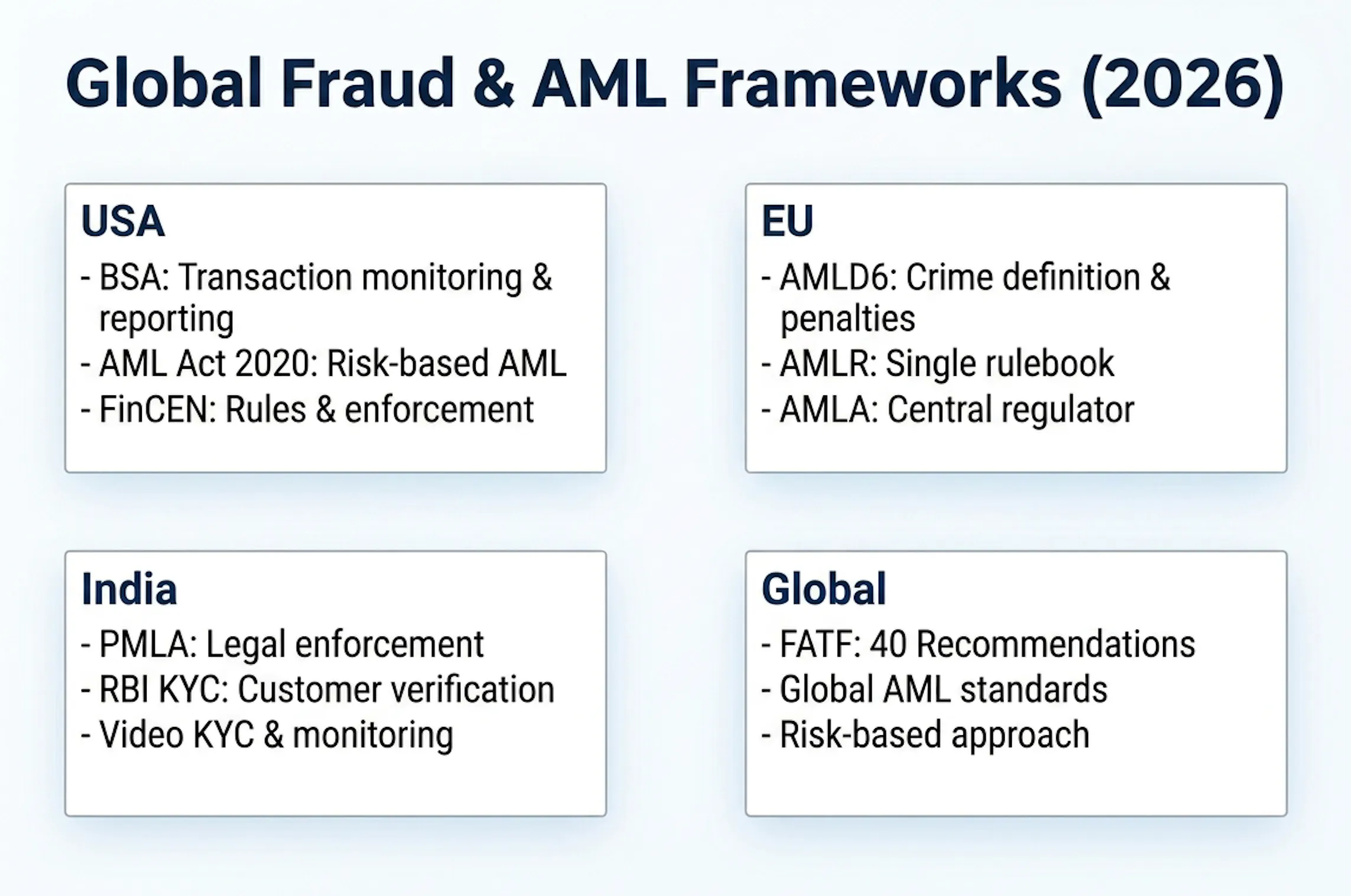

USA: Bank Secrecy Act (BSA), AML Act 2020, FinCEN rules

EU: AML Directives (AMLD6), upcoming AML Regulation (AMLR), AML Authority (AMLA)

India: PMLA, RBI KYC Master Directions

Global: FATF 40 Recommendations

Customer identity verification (KYC)

Transaction monitoring

Suspicious Activity Reporting (SAR)

Risk-based compliance programs

The BSA is the foundation of U.S. AML regulation, requiring financial institutions to:

Maintain records of financial transactions

Report suspicious activities (SARs)

Report large cash transactions (CTR)

Its core goal is to detect and prevent money laundering and fraud.

A major modernization of the BSA, this act:

Introduces a risk-based approach to AML compliance

Expands regulation to emerging sectors (e.g., crypto)

Encourages innovation (AI/analytics) in fraud detection

Focus shifts from compliance paperwork to effectiveness and risk management.

FinCEN (Financial Crimes Enforcement Network) issues detailed regulations under the BSA:

Customer Due Diligence (CDD) rules

Beneficial Ownership reporting

AML program requirements

FinCEN ensures institutions implement AML laws effectively and share intelligence with regulators.

AMLD6 is part of a series of EU directives that:

Define money laundering offenses and penalties

Expand liability to organizations and individuals

Focus is on harmonizing AML enforcement across EU member states.

AMLR will create a single rulebook across the EU:

Standardized KYC and AML requirements

Uniform compliance obligations for all countries

Removes inconsistencies between member states.

A new EU-level regulator that:

Oversees high-risk financial institutions

Coordinates cross-border AML supervision

Strengthens centralized enforcement and oversight across Europe.

India’s primary AML law that:

Criminalizes money laundering

Mandates reporting of suspicious transactions

Enables asset seizure and investigation

Focus is on legal enforcement and financial crime control.

Issued by the Reserve Bank of India, these guidelines:

Define customer identification (KYC) standards

Include Video KYC (V-CIP) and digital onboarding

Mandate ongoing monitoring of customer transactions

Ensure standardized customer verification across banks and NBFCs.

The global standard for AML/CFT (Counter Financing of Terrorism):

Sets risk-based approach principles

Covers KYC, reporting, sanctions, and monitoring

Guides national laws across countries

Countries align their regulations with FATF to avoid being grey-listed or blacklisted.

Regulators are moving away from checklist-based compliance toward performance-driven regulation.

In the U.S., FinCEN proposals emphasize how effective AML programs are, not just whether they exist

Enforcement actions increasingly focus on systemic failures, rather than minor technical lapses

Implication: Organizations must demonstrate measurable outcomes—like reduced fraud losses or improved detection rates.

Risk-based compliance is becoming a legal obligation, not just best practice.

Institutions must continuously assess and update risks based on customer profile, geography, and transaction behavior

Static, annual reviews are being replaced with dynamic, real-time risk assessments

Implication: Compliance programs must be adaptive and data-driven.

Regulators now expect organizations to adopt advanced technologies—but with accountability.

AI is being integrated into transaction monitoring, alert triage, and SAR drafting

In the EU, AI systems used in compliance are classified as high-risk, requiring strict governance and transparency

Implication: Firms must balance innovation with explainability and auditability.

Compliance obligations are no longer limited to banks.

Crypto exchanges, real estate firms, and even luxury sectors now fall under AML/KYC requirements

FATF’s Travel Rule is tightening requirements for digital asset transactions

Implication: A wider ecosystem must now comply with financial crime regulations.

Shell companies and hidden ownership structures are major fraud enablers. Regulators are addressing this by:

Expanding beneficial ownership reporting requirements

Increasing access to ownership registries

Mandating stricter due diligence

Implication: Organizations must dig deeper into who really owns and controls entities.

Fraud is borderless, and regulators are responding with cross-border cooperation.

Increased focus on information sharing between institutions

Joint enforcement actions across jurisdictions

Shared intelligence on fraud patterns

Implication: Siloed risk management approaches are no longer effective.

Different regions have overlapping and sometimes conflicting requirements, making compliance difficult for global firms.

AML compliance costs are rising significantly due to:

Technology investments

Skilled workforce needs

Reporting obligations

Traditional systems generate large volumes of alerts, many of which are false positives, reducing efficiency.

Fraudsters are leveraging:

AI-generated identities

Deepfakes

Synthetic fraud patterns

Compliance teams must constantly evolve to keep up.

Implement continuous risk scoring

Use behavioral analytics

Update models dynamically

Deploy machine learning for anomaly detection

Automate reporting workflows

Ensure explainable AI models

Use multi-source data (device, IP, behavioral signals)

Break data silos across departments

Train employees regularly

Foster a “compliance-first” mindset

Align fraud, AML, and risk teams

Maintain clear documentation

Enable audit trails for AI decisions

Align with global best practices

The regulatory environment in fraud and risk management is entering a new phase of maturity:

AI-driven compliance will become mainstream

Real-time monitoring will replace periodic reviews

Fraud and AML functions will merge into unified financial crime units

Regulators will demand proof of effectiveness, not just effort

In 2026, fraud regulation is no longer just about compliance—it is about capability, adaptability, and measurable impact. Organizations that treat compliance as a strategic function rather than a regulatory burden will be better positioned to:

Prevent financial crime

Build customer trust

Avoid penalties

Gain competitive advantage

If you want to learn more about M2P’s FRM & AML framework which is compliant and is implemented across mulitple markets and to explore how our capabilities can be tailored to your goals, we invite you to schedule a discussion with us.

Fintech is evolving every day. That's why you need our newsletter! Get the latest fintech news, views, insights, directly to your inbox every fortnight for FREE!