M2P Fintech

Fintech is evolving every day. That's why you need our newsletter! Get the latest fintech news, views, insights, directly to your inbox every fortnight for FREE!

The ambition to take a financial product beyond its native borders is the hallmark of a growing, forward-thinking fintech or enterprise. For those operating in the card issuance space, the mandate is clear: your customers are global, and your payment solutions must be, too. With the global prepaid card market projected to grow into a multi-trillion dollar industry by the end of the decade, the opportunity to deliver borderless, frictionless financial products is immense.

However, the journey from a successful domestic prepaid program to a truly global operation is rarely a straight line. It is fraught with regulatory hurdles, localized compliance mandates, and shifting consumer expectations. But beneath the surface of these visible challenges lies a much more insidious threat to your scaling ambitions - a silent operational killer that can drain your engineering resources and cripple your go-to-market speed.

We call it the Multi-Vendor Trap.

If you are currently evaluating how to take your prepaid program to the next country, region, or continent, understanding and avoiding the Technical Service Provider (TSP) Trap is the single most critical architectural decision you will make.

When you first launched your prepaid card program, you likely partnered with a regional Technical Service Provider (TSP) or issuer processor. This provider gave you the necessary APIs, handled the local regulatory compliance, and connected you to the domestic payment networks. It was the right move for that specific market. It allowed you to launch quickly, prove your product-market fit, and start generating revenue.

But what happens when you want to expand into a new region? Let’s say you are moving from the Middle East into Southeast Asia, or from India into the broader APAC market. The immediate, instinctual reaction for many product teams is to find a new, localized TSP in the target region. After all, a local provider already understands the local compliance nuances and has established banking relationships.

You sign a new contract, your engineering team begins integrating a brand-new set of APIs, and you launch. Then you expand to a third region, and the cycle repeats. On paper, you are a global prepaid program. In reality, you have fallen headfirst into the Multi-Vendor Trap.

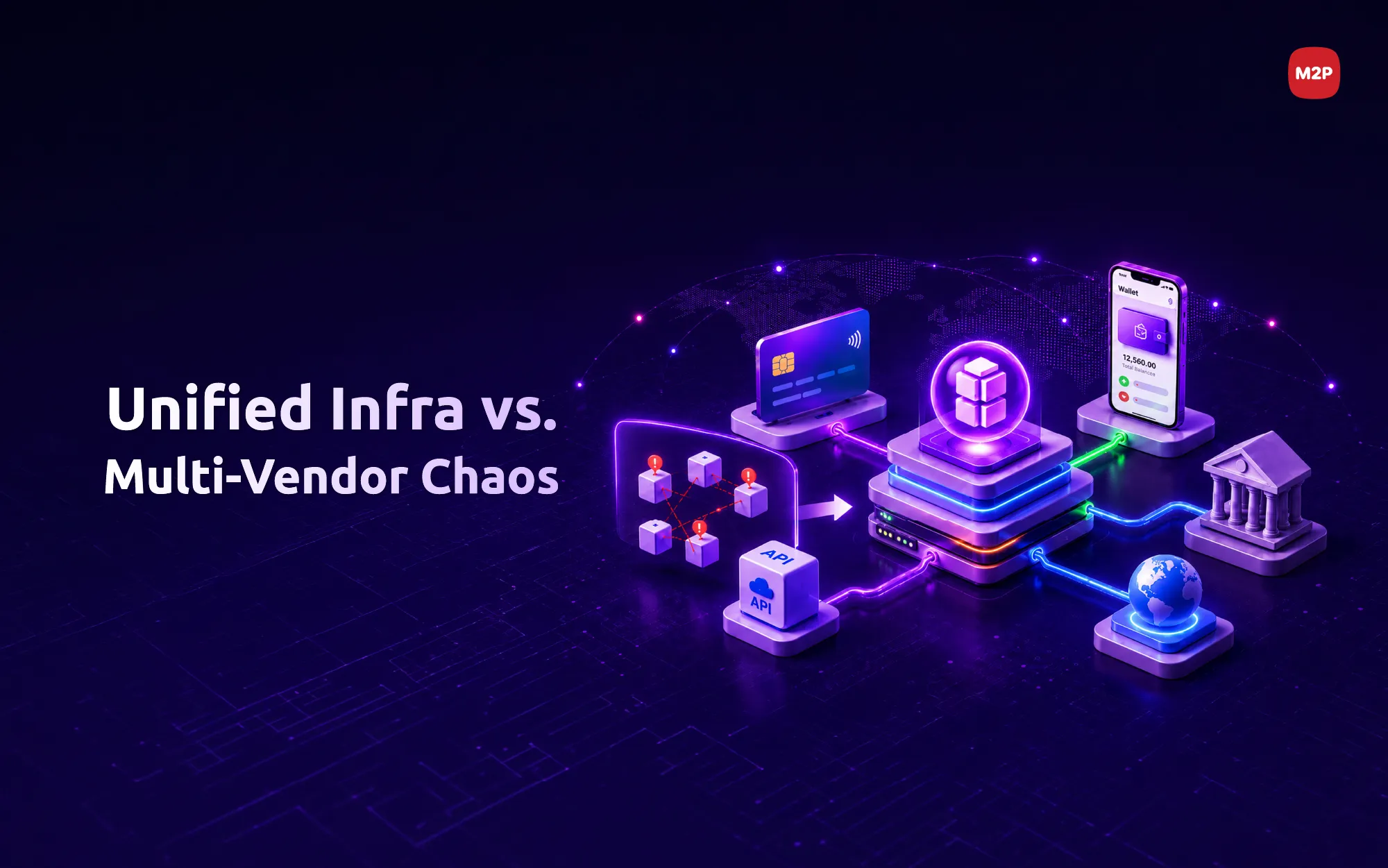

The Multi-Vendor Trap is the architectural and operational nightmare of stitching together multiple, disparate Technical Service Providers to power a single, theoretically "global" prepaid program.

Instead of building a cohesive, borderless financial product, you have inadvertently built a patchwork quilt of legacy systems, differing API standards, and siloed databases. You are no longer running one global program; you are operating three, four, or five entirely separate regional programs that just happen to share the same brand logo.

This trap is incredibly easy to fall into because it is disguised as the path of least resistance. Solving for one market at a time feels agile. But as you scale, the compounding tech debt of managing multiple TSPs will slow your innovation to a crawl.

The consequences of the Multi-Vendor Trap are rarely felt immediately. They creep in slowly, impacting every facet of your business from engineering to customer support.

First, consider the engineering resource drain. Every TSP has its own unique API documentation, sandbox environment, and integration quirks. Your developers, who should be building proprietary features that differentiate your product in the market, are instead relegated to API maintenance. Whenever a TSP updates their system or changes a security protocol, your team has to drop what they are doing to fix the integration. When you have four different TSPs, API maintenance becomes a full-time job rather than a routine task.

Second, the compliance and reporting chaos becomes overwhelming. Global financial operations require a single source of truth for reconciliation, fraud monitoring, and regulatory reporting. When your data is siloed across multiple regional processors, generating a unified global report is nearly impossible. Your finance team is forced to manually reconcile transactions across different dashboards, increasing the risk of human error and compliance breaches.

Finally, a fragmented backend inevitably leads to a fragmented user experience. If your European TSP supports real-time push provisioning to digital wallets but your Asian TSP does not, you are forced to either maintain different versions of your app or degrade the European experience to match the lowest common denominator. A modern user expects a fluid, identical experience regardless of their geographical location. This trap makes delivering that experience incredibly difficult.

To truly succeed on a global scale, you must shift your mindset from "multi-local" to "truly global." This requires an underlying architecture designed for scale from day one - a single, unified processing engine that abstracts the complexity of different regions away from your engineering team.

A unified platform gives you a single API endpoint to build against. Whether you are issuing a physical prepaid card in Dubai or generating a virtual, single-use token in Singapore, the API request looks exactly the same to your developers. The complexity of routing that request to the correct local bank, adhering to the specific regional KYC / AML rules, and settling the transaction in the correct currency is handled entirely by the platform, not your team.

This unified approach dramatically reduces your time-to-market for new regions. Instead of spending six to nine months integrating a new TSP, you can turn on a new geography through configuration rather than custom code. It allows your engineers to get back to doing what they do best: building exceptional user experiences.

At M2P Fintech, we recognized the limitations of the fragmented TSP model years ago. We knew that as embedded finance went global, businesses would need an infrastructure that could keep pace with their ambitions. That is why we built the M2P Prepaid Card Stack - a comprehensive, end-to-end operating system designed specifically for global scale.

Our platform is not a patchwork of acquired legacy systems; it is a unified, API-first architecture powered by our Turing orchestration engine. It centralizes product configuration, issuer processing, KYC, AML, and fraud controls into a single pane of glass.

When you build on M2P, you are integrating once for global reach. Our stack inherently supports sophisticated multi-currency wallets, enabling real-time currency conversion and automated transaction routing without requiring your team to build complex ledger logic. We have done the heavy lifting of establishing deep integrations with partner banks and global payment networks, giving you a ready-made global turnkey platform to launch physical, virtual, and tokenized cards.

Taking your prepaid program global shouldn't mean multiplying your operational headaches. As the landscape shifts toward an interconnected open finance era, the agility of your infrastructure will determine your market leadership.

Organizations that succeed will be those that view their underlying processor not as a utility, but as a strategic growth enabler. By choosing a unified API-first infrastructure over a fragmented collection of TSPs, you ensure your program remains resilient, compliant, and infinitely scalable. You are future-proofing your business against the complexities of cross-border finance.

Escape the TSP trap. Unbox your global potential. Let your technology be the engine of your expansion, not the anchor holding it back.

The global market waits for no one, and scaling on broken architecture will only cost you market share. If you are ready to ditch the integration headaches and launch your global prepaid program on a unified, proven stack - talk to us today.

Fintech is evolving every day. That's why you need our newsletter! Get the latest fintech news, views, insights, directly to your inbox every fortnight for FREE!