M2P Fintech

Fintech is evolving every day. That's why you need our newsletter! Get the latest fintech news, views, insights, directly to your inbox every fortnight for FREE!

Neo banks deliver digital banking services on steroids. The digital empowerment and financial possibilities they offer the underbanked and unbanked population are phenomenal. Their ability to foster financial inclusion with digitized convenience, lower cost, and personalized customer experiences are a few of the primary reasons for the success of neo banks in India.

Competing heavily on customer-centricity and deep tech, neo banks bridge the experiential gap between traditional banking services and evolving customer expectations. Free from legacy infrastructure hurdles, complex value chains, and stringent regulatory requirements, neo banks deliver super-fast, mobile-first services by leveraging advanced, agile, and lean business models.

In the next five years, the global neo bank market is slated to grow at 47.1% and hit $333.4 billion market size. In India too, neo banks are a thriving industry with a huge market potential of over 190 million unbanked/underbanked people who still need access to basic financial services.

So, if you are looking to set foot in the neo banking industry, this is the opportune time for you.

We are here to help you with step-by-step guidance.

Now, this is not unqualified guidance. We have immense experience and expertise in enabling neo banking services for leading players like Zenpay, Niyo, and Finin.

Let’s get started!

Step 1: Define target audience & value proposition

Step 2: Identify and analyze audience pain points

Step 3: Work on innovative, customer-centric strategies

Step 4: Build a strong core and backend infrastructure

Step 5: Focus on experience design

Step 6: Manage compliance and security

Step 7: Ease onboarding, engagement, and marketing

Fasten your seat belts!

Neo banks challenge the status quo of banking and payments for niche audiences. Hence defining that target audience is imperative to set up a neo bank.

For example, neo banks like FamPay cater to teenagers, and Zenpay caters to blue-collared workers. FamPay’s proposition comprises cards and bank accounts that teenagers can use under parental supervision. Whereas Zenpay offers payroll cards that provide blue-collared workers instant access to salary and incentives.

So, you need a crystal-clear understanding of your audience demographic and pain points to develop a value proposition accordingly. This will help you come up with a definitive reason why your customers should choose you.

Once your target audience is clearly defined, identify and analyze your target audience’s needs and pain points. This knowledge will help you include features that resolve audience issues, build trust and attract the right customer to your service. For example, Zenpay came at a time when the blue-collared workers were underbanked and were not able to access salaries and track their spending. The lack of access to salary accounts and other financial exclusion was the pain point for Zenpay’s audience. And their value proposition and services sought to resolve the challenge.

Looking at your target audience’s pain points and working to close the gaps is a key step while setting up a neo bank. This knowledge will help you differentiate and stand apart from other players in the industry.

Neo banks stand apart because of their agile, innovative, customer-centric business strategy. Leverage technology to make your business model and strategy as convenient and user-centric as possible. Pack in unique features that will get your customers coming back to you.

When it comes to features, some are must-have, and others are nice-to-have types. Must-have features are a necessity, without which the product or service will surely fail. Nice-to-have features are those that will add greater value and aid greater customer acquisition and retention.

Here are some examples for more clarity.

Low-cost structure

Easy money flow across borders

Quick account creation

User-friendly Interface

Real-time banking solution

High yield savings

Personalized card issuance (Physical/Virtual)

Zero joining fee

Zero annual Fee

Zero hidden Charges

Zero documentation

No-cost EMI

Personalized banking services

Educational loans/investments

Seamless budgeting

Tangible rewards

With advanced technologies such as Artificial Intelligence and Machine Learning ruling the neo banking industry, you can include new features, upgrades, and everything your target audience expects without any hassles.

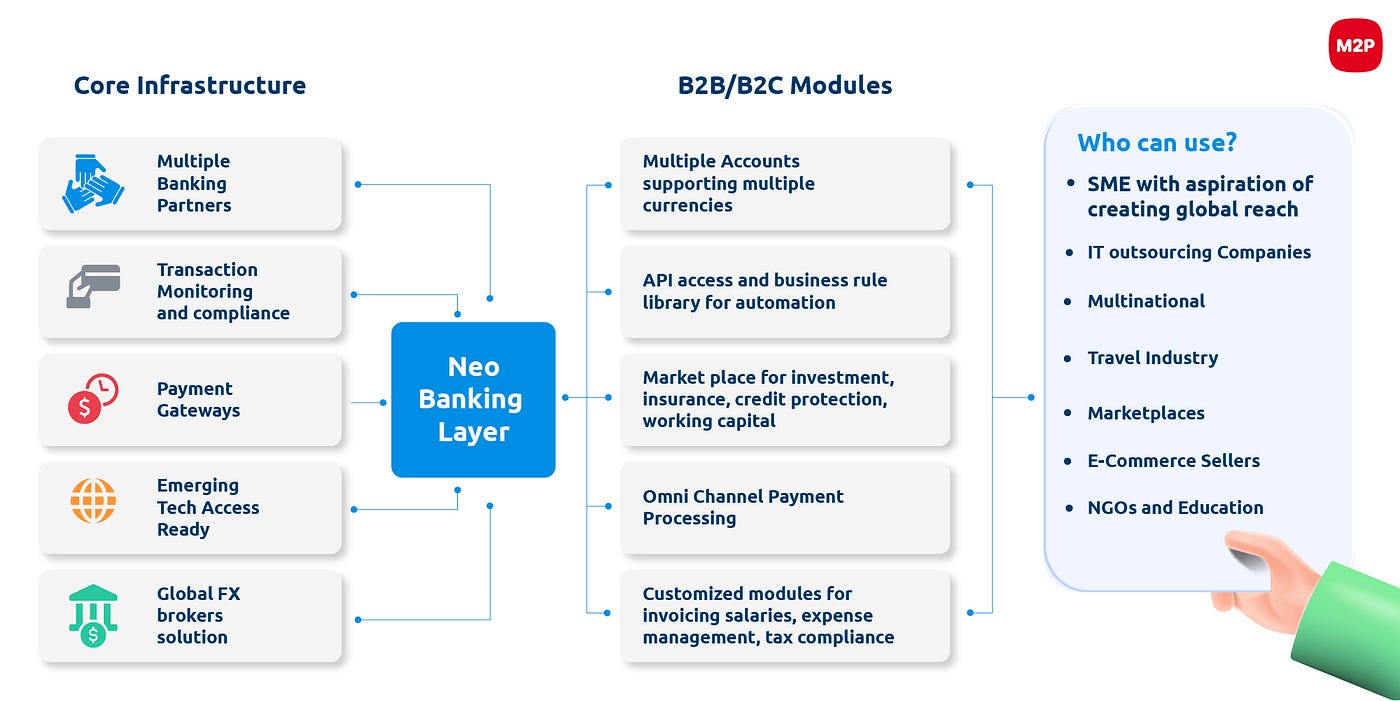

A robust neo banking app demands the best suite of core and back-end applications. As it has to deftly manage multiple applications and transactions without lags, the core and back-end infrastructure must be powerful enough.

To build a strong neo banking app, you need APIs, a card processing app, and back-office tools.

API: To connect your neo bank app with other services like payment gateway or authentication segment.

Card Processing App: This app is responsible for all the transactions or anything related to cards.

Back-office Tools: Manages the neo bank in the whole perspective.

The back-end infrastructure can be built in three different ways.

You require a banking license and a huge investment of time, effort, and money, as you are developing infrastructure, design, implementation, tech stack, and also the future sketch by yourself.

To minimize the time and effort, you can integrate with established banks and get your neo banking model started. It also does not require much work in terms of customer acquisition as you can leverage the bank’s trusted customers, to begin with.

You can partner with fintech companies to provide APIs to develop the core and bank end infrastructure for your neo bank. This decision with catapult your go-to-market speed to the next level with lower investment in terms of time and effort.

For example, fintech firms like M2P power neo banking apps by delivering tech stacks and best-in-class infrastructure to build customized products with seamless integration. We serve as an account aggregator of multiple banks and help neo banks leverage our partnerships and compliance to its best potential.

When it comes to card transactions, we take care of webhook notifications, reconciliation settlement, and even customer reports. For some of our neo banking customers, we also created co-branded debit cards with banks. We help them design their own debit card with features like multiple controls (PIN), lock/unlock cards, security measures, setting preferences, virtual cards, and more.

In India, neo banks do not work independently. Hence partnering with the right banks and API providers is critical to increase go-to-market speed and achieve growth and profitability.

Humanizing transactions and enabling personalized experiences is key for the success of a neo banking app. To that end, you need to prioritize experience design for visually appealing app design and easy-to-understand interfaces and clear call-to-action.

Experience design enables frictionless navigation and improves customer experience by focusing on speed, convenience, security, and seamlessness. Ensure your neo banking apps are aesthetically designed for a smooth customer journey and satisfaction.

Better the security, better the trust!

Regulatory compliance and security infrastructure design play a significant role in neo banks, as customer data and money are at stake here. Managing PCI DSS compliance, tokenization, the generation and issuance of payment tokens, and the operation and maintenance of a token vault is a laborious yet critical process.

Hence, start with setting up the Security Office Center (SOC), which will function as a command center for your neo bank app. This helps you in analyzing every crumb of information in your infrastructure. You can even implement Security Information and Event Management (SIEM) software solution to secure and analyze every activity in your neo bank.

You can even go the extra mile by building your own security tools and solution to protect customer data. It is highly advisable to maintain access logs or anything happening in your neo bank platform to have a record for your security team to look into any time in the future.

Before stepping onto the deployment stage of your neo bank, run a series of checks and automated tests to identify and get rid of the issues. Think of every possibility your user may utilize your app for. Here’s a series of tests you can opt for:

Unit-testing

Integration testing

Security testing

User acceptance testing

Regression testing

Ensure your team runs the tests even after the app goes live because this lowers the chance of your app facing security issues later. Automating the tests by implementing a custom infrastructure helps in this case.

Fuse security onto DevOps — DevSecOps to develop your neo bank application. At the time of upgrades and new releases, you can go to market quickly and seamlessly.

Don’t just sit back after launching your neo bank. Your journey has only begun.

Ensure onboarding is simple, smooth, and effortless for customers. Focus on marketing efforts to acquire and retain customers. Ensure you engage your customer throughout their journey with your neo bank.

Remember, the profitability of your neo bank can be determined by the customer Life-Time Value (LTV)/ Customer Acquisition Cost (CAC) ratio. The higher the LTV/CAC ratio, the greater will be the income generated per new customer. So, the key is to keep your customers happy.

All set to start your own Neo bank? Got more questions in your mind?

Ping us at business@m2pfintech.com.

Subscribe to our newsletter and get the latest fintech news, views, and insights, directly to your inbox.

Follow us on LinkedIn and Twitter for insightful fintech tales curated for curious minds like you.

Fintech is evolving every day. That's why you need our newsletter! Get the latest fintech news, views, insights, directly to your inbox every fortnight for FREE!