M2P Fintech

Fintech is evolving every day. That's why you need our newsletter! Get the latest fintech news, views, insights, directly to your inbox every fortnight for FREE!

Lending is a complex world where loan origination to disbursal is a sea of procedures. It involves tremendous efforts, time, and logistical investments from the loan seeker. Right from KYC verification to document submission, loan application form & user-setup, account mandates, amount sanction, and disbursement, end-use monitoring & EMI/Principal collection, the entire life cycle of the loan is mostly offline.

It paves the way for many instances of fraud/mis-governance, data input error, transaction failures, other issues, and loan closure inconsistencies. It also prevents many from seeking credit as they are wary of these cumbersome procedures.

Sunil is an MSME entrepreneur, residing in a semi-urban area called Bandipur. He ran a profitable electronic shop before being railroaded by the pandemic. The business faced a looming loss and a climbing expense due to strict lockdown measures. Since most of the lenders were in the urban or metropolitan cities, he had limited credit options.

In fact, from March 2020, Sunil was finding ways to avail credit. He had made endless negotiations with lenders available, expecting a reasonable rate and term. It was a fruitless quest; Sunil had to get a loan from a lender named Roy Chatterjee, at very high interest. He completed all the steps from risk assessment, KYC verification, credit assessment, loan disbursement, and collection offline.

In the process, Sunil discovered that having minimal or almost no digital facility in the loan application method had given him a suboptimal output. The lending life cycle was complex and filled with data input errors, transaction failures, and loan closure inconsistencies.

He also arrived at the conclusions that:

The absence of data yielded him risky credit allocation and disbursement

Secondly, the lack of digital infrastructure led to increased inconvenience

Owing to a lack of repayment data, the lender misleadingly showed several months of missed collection and charged more than the actual amount. So, Sunil ultimately had to shut down his business and sell his assets for loan closure.

What would have saved Sunil’s business?

The availability of competitive Digital Credit or Lending Solutions from various lenders could have given Sunil the right credit options.

Sunil’s dilemma is an example of the current MSME situation in India. The MSMEs are referred to as the Lost Middle as their needs are not addressed. Their distinct requirements fall between microcredit organizations like Micro-Finance Institutions (MFINs) and banks, thereby making them prey to secondary lending agencies who charge exorbitant interest rates and sometimes deceive. And that’s where platforms like OCEN comes in as a helping hand.

OCEN stands for Open Credit Enablement Network. It aims to promote transparent loan origination and participation from categories of Education, e-commerce, Payment Aggregators, Fintechs, and NBFCs. This platform is designed to serve even niche customers or borrowers like Sunil.

Fundamentally, OCEN is the brainchild of iSpirt, Sahamati, and Credall. It is a digital lending solution that provides credit to customers having a credit history and provides micro-credit opportunities to people with no credit or bank transaction history. In short, the platform aims to improve and enable credit access to everyone.

Generally, it targets to serve all possible borrower categories like personal, home loan, and business. Furthermore, it offers a marketplace model for loan offerings.

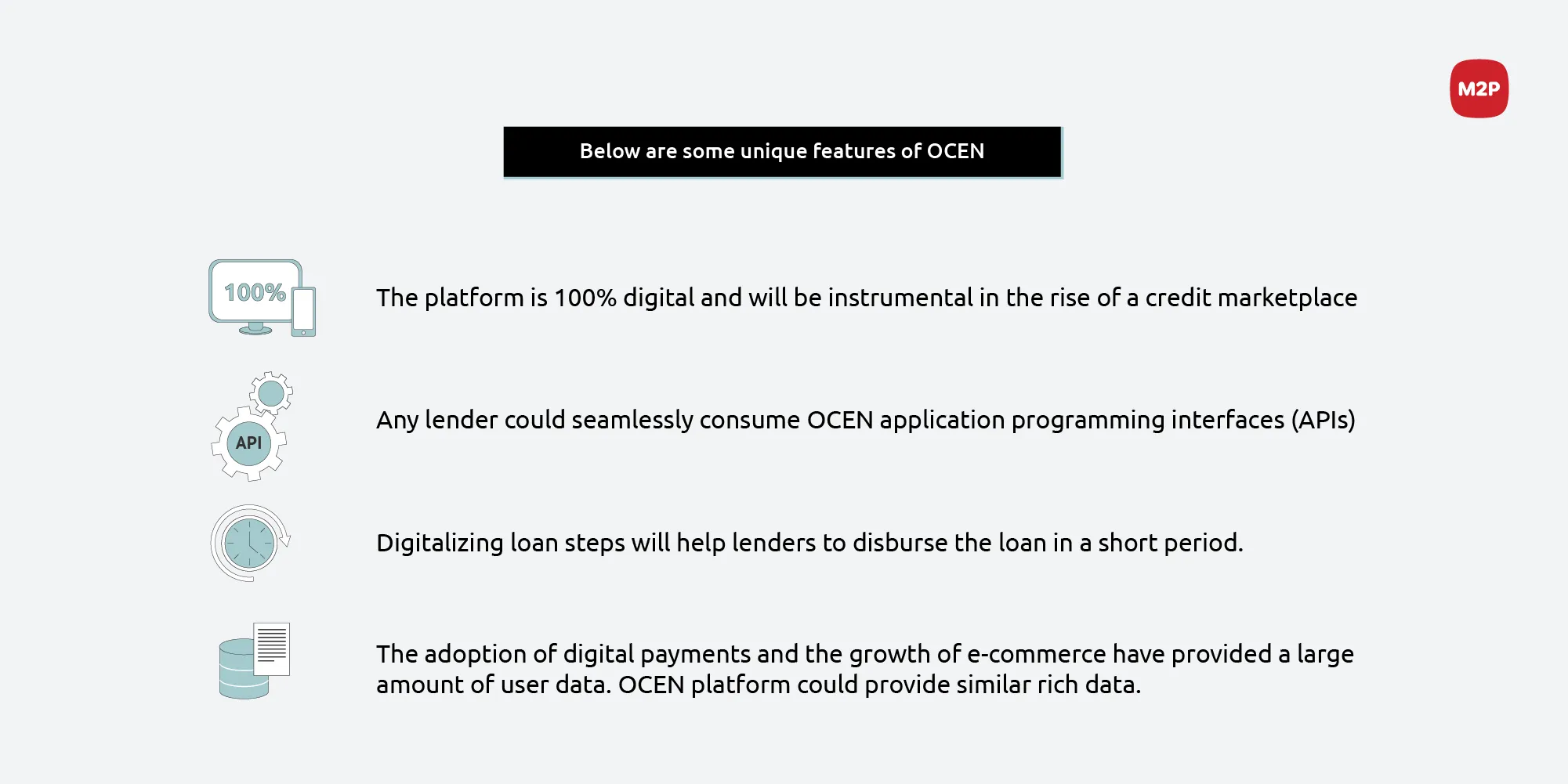

OCEN aims to resolve the major problems by emphasizing Digital-Only assessment, sanction, and disbursement of loans to borrowers. It supports borrower and lender usage monitoring, thereby ensuring a 360° data collection and analysis.

Digital lending can prevent mis-governance or fraudulent loan practices by both the parties — loan seeker and loan provider.

OCEN is best suitable for MSMEs because its open protocols will ignite further innovation at each step of the loan process. Furthermore, it will help to democratize credit. It can even ensure that every service provider offers credit by just plugging into the platform.

Yes. It can rapidly increase credit availability to enterprises that are already digitized to a greater extent. For other MSMEs that operate in a minimum data zone or with a low digital base, lenders need to utilize the physical and digital infrastructure and channels. Simply put, overcoming data errors or discrepancies for companies with a minimum digital capability is still an issue to be addressed.

OCEN is expecting to terra-form the credit landscape in the coming months and years ahead. It will allow small businesses to avail credit in real-time. Whether its supply chain finance for broad/long term or instant-short term credit or any other trade-specific condition, you could anticipate a sea-change transformation in the more extensive credit process.

The next visible step in OCEN — is the significance and authorization of Loan Service Providers (LSP) categories. Finally, the rationale behind the digitalization of lending and the Open Credit Enablement Network is to make “Credit for Everyone” a reality.

Subscribe to our newsletter and get the latest fintech news, views, and insights, directly to your inbox.

Follow us on LinkedIn and Twitter for insightful fintech tales curated for curious minds like you.

Author- Abhishek Mody

Fintech is evolving every day. That's why you need our newsletter! Get the latest fintech news, views, insights, directly to your inbox every fortnight for FREE!