M2P Fintech

Fintech is evolving every day. That's why you need our newsletter! Get the latest fintech news, views, insights, directly to your inbox every fortnight for FREE!

The world of banking has transformed over the years. Customer experience has now become a key differentiator. Personalization, speed, convenience, and security have evolved as factors that determine profitability.

To keep pace with the changing customer expectations and the competitive landscape, banks need to modernize their core banking systems. Only then can they scale technology innovation, upgrade processes, and re-engineer their workforce to deliver mobile-first, personalized customer experiences while reducing cost and complexities.

Go beyond the surface and explore more.

Centralized Online Real-time Environment (CORE) banking systems serve as the technical infrastructure that enables banks to manage their day-to-day operations efficiently and seamlessly. They facilitate branch agnostic transactions across multiple touchpoints worldwide.

Hosted on-premise or in the cloud, core banking provide a singular view of customer data to facilitate information flow and operational excellence across delivery channels. It simplifies services such as new account creation, customer relationship management, transaction processing, loan issuing, and servicing. Banks can achieve greater cost and operational efficiencies by making the big shift from legacy to modern core banking solutions.

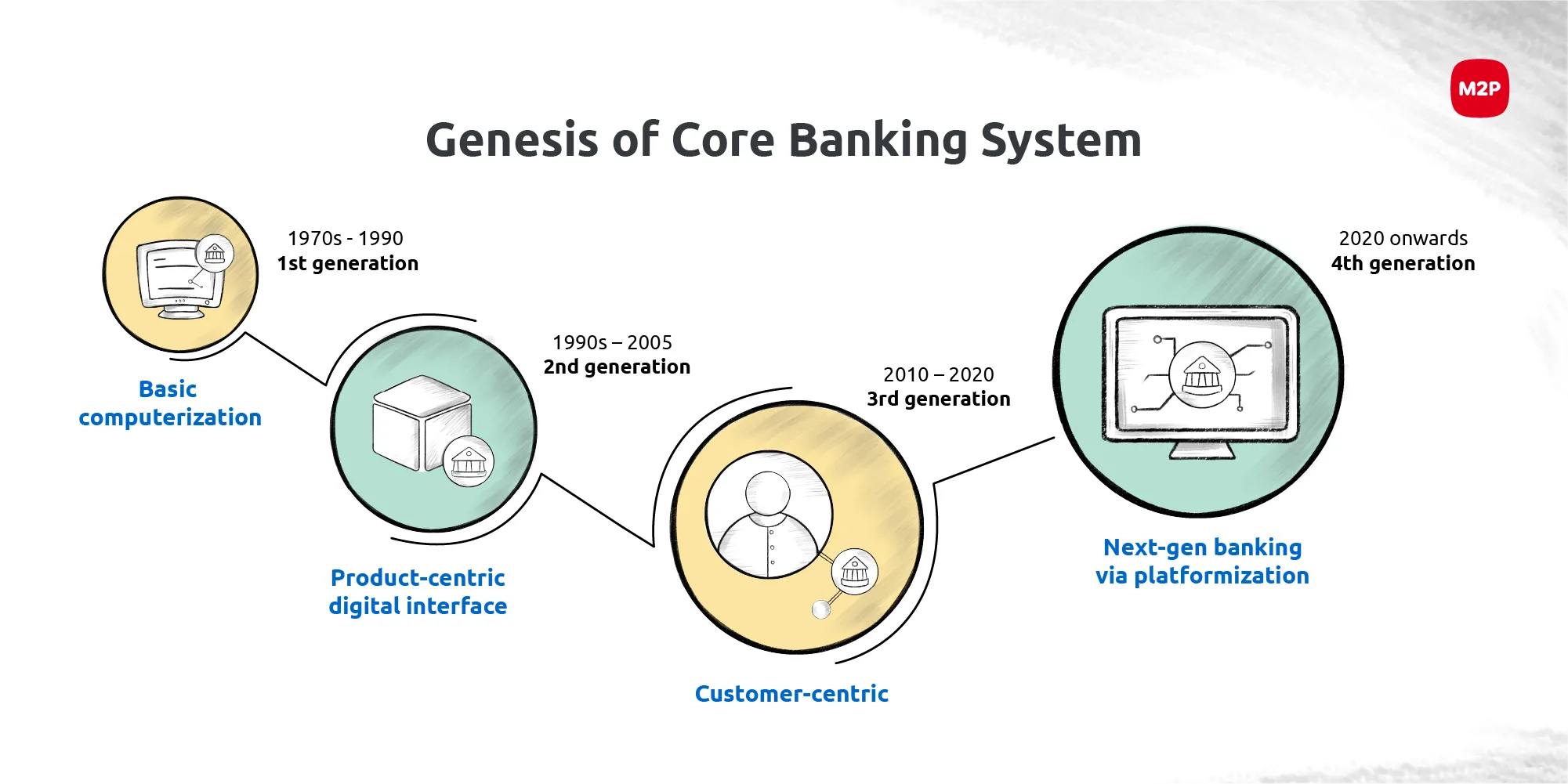

Core banking is not a new phenomenon. It had a humble beginning in the 1970s with rigid codes and basic computerizations and evolved with technological advances, product innovations, and customer requirements to be what it is today.

From 1970 to 1990 CBS began taking root in the banking industry. At its most primal form, the system functioned on basic computerization techniques and was developed in-house by most banks.

The 1st gen CBS used monolithic applications that were based on complex codes. The IT costs were quite high, and it offered only a few basic features like transaction execution, record-keeping, and customer data management. Sequential data were stored in silos, and transactions were processed in batches at the end of the day.

So, money transfers and payments could not be processed in real-time. The applications were accessible to users only during counter hours. The system was prone to data loss and was difficult to replace without causing a service disruption.

From 1990 to 2005, CBS was in its product-centric avatar with a penchant for digital interfaces. The infrastructure developments were outsourced to external parties that focused on building a vibrant user interface for 24/7 access to banking services.

Software modules and a few subroutines were introduced to improve the flexibility of the code. But, even after several optimization trials, the code remained complex. This made processing large volumes of transactions tougher. And banking data were still organized in silos.

Client programs were slowly added even though the standards were still mainframes. Software that was previously accessible through branch networks now became available to customers at ATMs and payment terminals. However, during maintenance, the system still faced prolonged service disruption.

2010 was the year 3rd generation CBS came into prevalence. It was a major leap from the yesteryear computerizations and product-centric interfaces. CBS became more customer-centric, and banks began building a digital layer to improve flexibility.

The first programming interfaces appeared, and the core banking software was accessible on the Internet. The software architecture became less monolithic, and the system started to adapt to newer structures, such as Application Service Providers (ASPs) and Service-Oriented Architectures (SOAs).

On the user experience side, newer milestones were achieved, and now version changes could be performed in a shorter span of time. Truly graphic interfaces in HTML and Windows pages were introduced.

The infrastructure was completely customer focused. But things started to change when the pandemic struck in 2020. Customer needs, expectations, journeys, and touchpoints underwent a radical transformation.

Modern core banking systems came around to save the day. It kickstarted digital transformation in traditional banks and helped new-age banks accelerate next-gen customer experience. API-led core banking architectures enable banks to scale reliable and strong banking ecosystems with frictionless, rapid integrations.

After 2020, 4th generation core banking systems came into prevalence. Platformization of CBS evolved as a crucial development, transforming the core from being only a system to becoming a complete platform.

Going beyond traditional models, modern core banking platforms give banks the agility to scale and fully leverage the potential of digital revolution to satisfy stakeholders such as customers, employees, regulators, and partners. However, traditional banks with legacy core banking platforms still grapple with silos, code rigidity, and complexities. Even though their financial processes are automated and newer distribution channels are in place, legacy systems hinder adaptive flexibility to changing customer journeys and behavior, closed ecosystems, and vendor lock-ins. They also result in higher maintenance costs, slower GTM speed, and do not support instant releases.

Next-generation core banking platform breaks down all the barriers that legacy systems impose. They accelerate digital transformation using modern, scalable, and open architectures and lightweight codes. Leveraging APIs and advanced technologies like machine learning, core platforms deliver simplicity, cost efficiency, speed, interoperability, flexibility, security, and future readiness.

Simplicity in scaling up

Agility to accelerate new product launches

Incredible go-to-market speed

Onboarding and setting up happen in a few clicks

Advanced security systems for data storage and fraud prevention

Centralized access to account aggregators, mobile and third-party applications

Turing Core Banking System (CBS) is a next-gen platform that focuses on customer experience, operational excellence, and security well within the regulatory framework. It is built on the latest micro-services architecture with low code and an API-first, cloud-agnostic platform making it a modern and futuristic core banking system.

Incredible Speed of innovation (using AI and ML)

Flexibility (low code capabilities)

Agility (hyper-personalized products)

Pre-integrated with Fraud Risk Management (FRM) engine

Furthermore, the primary vantage point of 4th Generation CBS is its ability to evolve and adapt to emerging trends in the financial industry.

Open banking and the utilization of APIs are key drivers in the next generation of core banking platforms. APIs empower financial institutions to seamlessly integrate with third-party banking solutions, enhancing their service offerings and expanding their reach within the digital ecosystem. This synergy facilitates innovation and the creation of a comprehensive banking experience.

The integration of artificial intelligence (AI) and machine learning revolutionizes core banking software. These technologies provide predictive analytics, bolster fraud detection, and deliver personalized customer experiences. Harnessing the insights from vast data pools, AI and machine learning empower banks to make informed decisions, streamline operations, and foster heightened customer satisfaction.

As digital transactions become more common, security remains paramount. Multi-layered security protocols, including biometric authentication, two-factor authentication, and end-to-end encryption, are being woven into the fabric of core banking systems. These measures are crucial in safeguarding sensitive customer data and maintaining trust in an increasingly digital landscape.

Modern core banking software centers on user-centric design principles. Intuitive interfaces, personalized dashboards, and mobile responsiveness are integrated to ensure that both bank employees and customers enjoy a seamless and intuitive banking experience.

The evolution of core banking goes beyond technological advancements and encompasses sustainability, embracing the principles of green fintech. Core solutions align with global concerns about climate change and social responsibility by integrating features that facilitate green investments and enable carbon footprint tracking.

Blockchain technology and cryptocurrencies are reshaping the financial system. Some core banking software is now incorporating DeFi integrations, enabling banks to offer services related to crypto trading, lending, and borrowing.

Voice assistants and chatbots are being integrated into banking systems to provide instant customer support and assist with transactions. Customers can perform banking tasks using natural language, simplifying interactions, and reducing the need for manual assistance.

The future of banking is driven by digital innovation, connectivity, and a steadfast focus on customers. Modernizing the core is no longer a choice, it is a dire requirement for banks to grow with agility, efficiency, and customer-centricity.

Want to know more about modernizing your core banking system?

Write to us at business@m2pfintech.com.

Subscribe to our newsletter and get the latest fintech news, views, and insights, directly to your inbox.

Follow us on LinkedIn and Twitter for insightful fintech bytes curated for curious minds like you.

Fintech is evolving every day. That's why you need our newsletter! Get the latest fintech news, views, insights, directly to your inbox every fortnight for FREE!